[1945002WorkingCapitalfürkleineUnternehmen] the following article is contributed by Rober Glör of IOU Central, a provider of short-term loans. The discussion on the simple interest as compared to pre-computed interest is very interesting.

I was shocked that some businesses effectively their loans small businesses punished for paying off early by a higher effective interest rate charge.

Chances are, as a small business owner, you know that a bank loan is getting nowadays not very easy. In fact, the number of small businesses is still at below levels prior loans in the United States the recession.

An important reason for this is placed the strict regulation of traditional banks. For example, does the work hours when processing a small business loan application involved just the return on investment was too low. many banks can not make money at all by lending to small businesses, in fact. As a result, many small businesses have need loans for things like the expansion to increase to a larger location or inventory seize the opportunity had to look outside of traditional banks.

Fortunately, there are alternative lending options, many of which are of very reputable lenders offering competitive rates for small business loans. That being said, it is important to do your homework on the different lenders and make sure you understand the fine print on their total costs.

Need some money for your business? Click here to get our free guide:

How to get a Small Business Loan

All interest rates are not the same

There are three. main types of alternative credit products. Most borrowers are looking for the lowest interest rate but not truly understand what it could mean the particular type of interest or factor rate to the total cost over the life of the loan. Let's take a closer look at three different types of alternative credit products and the difference between them:

1. A merchant cash advance or MCA: This is where the company buys your future credit card receivables at a discount. The average or typical MCA product generally carries a 1.38 factor rate and the repayment is usually set to faster than the typical pre-calculated or simple interest loan product.

(for proceeds means $ 100,000 you are $ 138,000 to repay) 2. Pre-computed interest business loans: With this approach, the interest payments for the entire duration of the loan are calculated in advance from the date the you borrow and added to the total loan amount. This calculated interest shall be payable over the term of the loan and will not change. The disadvantage of this approach is that even if the loan is paid in advance, the full interest needs to be paid in full.

3. Simple Interest: This approach calculates the interest due on the loan by the principle balance outstanding every day. Therefore, as the loan amount decreases (usually daily with a daily credit payment), also notes the interest.

The awareness of the various interest rate options can help small businesses to save money and is crucial in determining how much you are actually paying for the loan total.

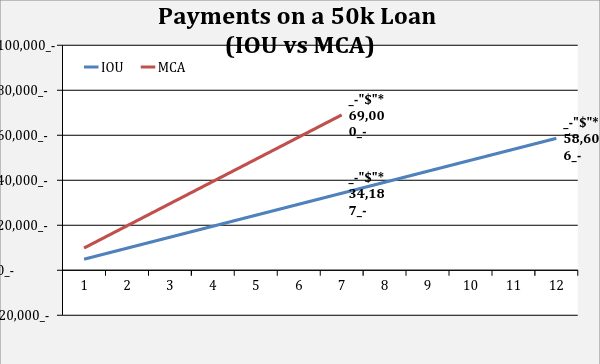

the example of John Smith, owner consider a pizza means to illustrate. Let Johns furnace breaks say significantly affect its ability to serve customers. He needs a loan quickly and know that a traditional bank loan will take too long to secure. He also knows he has a good chance to be refused, despite its excellent credit. John comes two alternative lenders, an offer merchant cash advance and the other with simple interest. Let us see in the overall total cost of Johns $ 50,000 loan on the difference: (With an average risk IOU Central Client vs 1.38 7 months MCA Factor transaction)

How may look different, the total cost of the loan may be based heavily on the type of financing product. It is as simple as the question which is kind of interest on a loan? Here are some additional questions to ask your lender that you and help uncover the true overall cost of your small business loans save money:

-

, including all fees and interest - what is my TOTAL COST for the funds? (To a factor rate comparison, divide the sum of the payments in the net loan amount on each of the transactions to calculate try compare)

-

How long or what my expected life? When I pay my mortgage in advance, I'll pay less interest or get a reduction in my entire repayment?

The good news is that there are options these days for small business loans outside traditional banks. While alternative lending options to navigate and understand, require their conditions some efforts can go a little knowledge to save a long way to make money. And that is money that you can grow elsewhere for your business.

About the author

Need some money for your business? Click here to get our free guide.

How to get a Small Business Loan

0 Komentar